")

In today’s dynamic financial landscape, astute homeowners are constantly seeking avenues to optimize their assets and enhance their financial flexibility. A home equity line of credit (HELOC) can be a powerful tool, providing access to liquid funds tied to your home’s value. However, as market conditions evolve and personal financial goals shift, the question often arises: can you refinance a home equity line of credit to better suit current circumstances? In this article, Daily98news will accompany you to explore this critical aspect of homeownership and investment strategy, offering an in-depth analysis grounded in financial discipline and market expertise. Understanding the mechanisms and benefits of refinancing your HELOC is paramount for maintaining robust financial control and adapting to economic changes effectively.

Understanding Home Equity Lines of Credit (HELOCs)

A Home Equity Line of Credit, or HELOC, represents a revolving line of credit that utilizes your home’s equity as collateral. Similar to a credit card, it allows homeowners to borrow funds as needed, up to a predetermined maximum credit limit, and you only repay the amount you actually use. HELOCs are typically structured with a variable interest rate, meaning the interest you pay can fluctuate with market rates, often tied to the U.S. Prime Rate. This flexibility makes them attractive for ongoing expenses, such as extensive home renovations, educational costs, or consolidating higher-interest debt. The typical HELOC structure involves a “draw period,” usually lasting around 10 years, during which you can access funds, make interest-only payments, and repeatedly draw and repay within your credit limit.

Following the draw period, the HELOC transitions into a “repayment period,” where you are typically required to make principal and interest payments over a set term, often 10 to 20 years. This shift can significantly increase monthly payments, particularly if borrowers made only interest-only payments during the draw phase or if interest rates have risen. The variable nature of HELOC interest rates, while offering potential savings in a declining rate environment, also exposes borrowers to the risk of rising costs when rates climb. Maintaining a clear understanding of these phases and their financial implications is essential for any homeowner utilizing a HELOC.

Why Consider Refinancing Your HELOC?

The decision to refinance any loan is driven by a desire for improved financial terms or greater flexibility, and a HELOC is no exception. Several compelling reasons might lead a homeowner to ask, can you refinance a home equity line of credit. One primary motivation is a change in the interest rate environment. If you secured your HELOC when interest rates were high, a subsequent decline in market rates could present an opportunity to refinance into a new HELOC with a lower annual percentage rate (APR), thereby reducing your overall interest costs and monthly payments.

Another significant factor is the transition. Refinancing at this juncture can help manage these higher payments by potentially securing a new draw period or converting to a fixed-rate loan with more predictable installments. Furthermore, an improved personal credit profile or a substantial increase in your home’s equity since the original HELOC was established can enhance your eligibility for more favorable terms, including lower rates or a larger credit limit. Debt consolidation, streamlining finances, and achieving greater payment predictability are also powerful incentives for exploring refinancing options.

Key Options for Refinancing Your HELOC

When considering whether you can you refinance a home equity line of credit, it is crucial to understand the various pathways available, each with its unique characteristics. These options offer different structures and benefits, allowing homeowners to select the best fit for their financial strategy and current market conditions. The choice often depends on whether you seek continued flexibility, predictable payments, or a consolidation of your home-related debts.

There are three primary methods homeowners typically explore to refinance a HELOC:

Refinancing into a new HELOC

This option involves replacing your existing HELOC with a brand new one, potentially, a consideration for long-term financial planning.

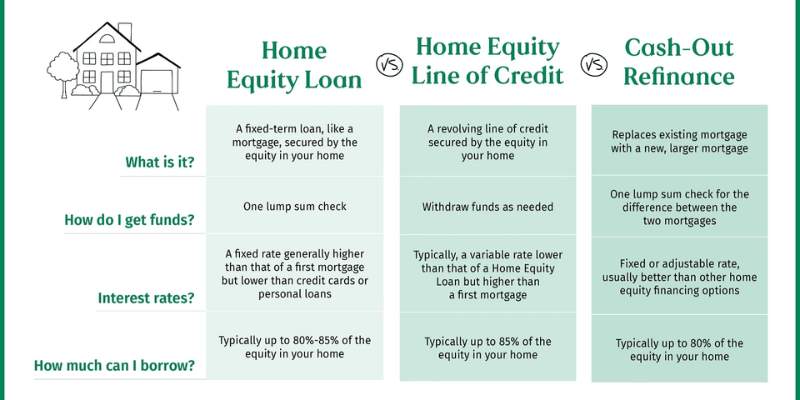

Refinancing into a home equity loan

Unlike a HELOC, a home equity loan provides a lump sum of money upfront with a fixed interest rate and a set repayment schedule. This predictability can be highly appealing, especially if your current HELOC has a variable rate that has increased or is projected to rise. By converting your HELOC balance into a fixed-rate home equity loan, you lock in a stable interest rate and consistent monthly payments, making budgeting simpler and providing protection against future rate hikes. This option is ideal for those who have a specific amount they need to repay and prefer the security of fixed installments rather than the variability of a HELOC.

Refinancing with a cash-out refinance

A cash-out refinance involves replacing your existing first mortgage with a new, larger mortgage, and using the difference to pay off your HELOC and potentially receive additional cash. This approach consolidates your primary mortgage and your HELOC into a single loan with a single monthly payment, simplifying your debt structure. It can be advantageous if current mortgage rates are lower than your existing primary mortgage rate and your HELOC rate, potentially leading to lower overall interest costs and more manageable payments. However, a cash-out refinance resets the term of your entire mortgage, which could mean paying interest over a longer period, and typically involves closing costs similar to those of your original mortgage.

The Refinancing Process: What to Expect

Embarking on the journey to refinance a home equity line of credit requires careful preparation and an understanding of the steps involved. This process is similar in many ways to obtaining your initial mortgage or HELOC, demanding diligence in documentation and a clear assessment of your financial standing. Knowing what to expect can help streamline the application and approval phases.

The general steps for refinancing your HELOC typically include:

- Evaluating your financial health: Lenders will scrutinize your credit score, debt-to-income (DTI) ratio, and payment history. A strong credit score, ideally 680 or higher, can significantly improve your chances of securing a lower interest rate and more favorable terms. Lenders generally prefer a DTI ratio of 43% or lower to assess your ability to manage new payments.

- Assessing your home equity: You will need sufficient equity in your home to qualify for refinancing. Most lenders require a certain loan-to-value (LTV) ratio, often desiring at least 15-20% equity remaining after the refinance. An updated home appraisal will likely be required to determine your home’s current market value.

- Shopping for lenders: It is highly advisable to compare offers.

- Application and documentation: Once you select a lender, you will complete a formal application and provide necessary documentation, which may include proof of income, tax returns, bank statements, and details about your current HELOC and primary mortgage.

- Closing costs and fees: Refinancing, like any new loan, typically involves closing costs. These can range from 1% to 5% of the total loan amount and may include appraisal fees, origination fees, title insurance, and legal fees. Some lenders may offer “no closing cost” HELOCs, but these often come with higher interest rates. It’s crucial to factor these costs into your calculations to determine the true benefit of refinancing.

Pros and Cons of Refinancing Your HELOC

Deciding whether you can you refinance a home equity line of credit involves a thorough evaluation of the potential advantages against the inherent disadvantages. This balanced perspective is crucial for making an informed financial decision that aligns with your long-term wealth management goals.

Advantages

- Lower interest rates: If current market rates are lower than your existing HELOC rate, refinancing can significantly reduce the interest you pay over the life of the loan, leading to lower monthly payments. For instance, the national average HELOC interest rate was 7.81% as of November 12, 2025, a notable decrease.

- Fixed interest rates: Many HELOCs have variable rates, exposing you to market fluctuations. Refinancing into a fixed-rate home equity loan provides predictability and stability, protecting you.

- Reduced monthly payments: By securing a lower interest rate or extending the repayment term, refinancing can decrease your monthly financial obligations, freeing up cash flow for other investments or expenses.

- Restarting the draw period: Refinancing into a new HELOC can provide a fresh draw period, granting you continued flexible access to funds for future needs.

- Debt consolidation: Consolidating higher-interest debts into a new HELOC or a cash-out refinance can simplify your finances and potentially reduce your overall interest burden.

Disadvantages

- Closing costs: Refinancing is not free. You will incur various closing costs, which can range from 1% to 5% of the new loan amount, potentially offsetting some of the interest savings, especially if you plan to move or repay the loan quickly.

- Resetting the loan term: If you opt for a cash-out refinance that includes your primary mortgage, you will reset the repayment clock on your entire mortgage. While this can lower monthly payments, it might also mean paying interest over a longer period, increasing the total interest paid over time.

- Potential for higher rates: If interest rates have risen since you first obtained your HELOC, refinancing might result in a higher rate, increasing your monthly payments. It is essential to carefully evaluate current market conditions before proceeding.

- Risk to home equity: As with any loan secured by your home, failing to make payments could put your property at risk of foreclosure. Refinancing involves taking on new debt, and it should only be undertaken if you are confident in your ability to meet the new repayment obligations.

- Early closure fees: Some HELOCs include early closure fees if the line of credit is paid off and closed within a certain timeframe, typically the first few years.

Navigating the Market: Strategic Timing for Refinancing

The timing of a refinancing decision for your HELOC is critical and should be informed by a comprehensive understanding of macroeconomic trends, particularly interest rate movements. As a seasoned financial analyst, I emphasize that market assessment goes beyond mere observation; it involves anticipating future shifts and positioning your portfolio accordingly.

Currently, the Federal Reserve has been navigating a complex economic landscape, with interest rate policy being a key tool to manage inflation. Recent Federal Open Market Committee (FOMC) projections indicated that rates would likely end 2025 between 3% and 4%, with a bias towards the lower end of that range. Indeed, the Fed has implemented rate cuts in September and October 2025, bringing the federal funds rate to a target range of 3.75%-4.00%. Goldman Sachs Research, for instance, projects a likely December rate cut as well, with further cuts in March and June 2026, targeting a terminal rate of 3-3.25%. These anticipated rate cuts generally translate to lower borrowing costs for consumers, including those on variable-rate HELOCs, or potentially more favorable terms on fixed-rate alternatives. For example, the national average HELOC rate dropped to 7.81% as of mid-November 2025, reflecting a significant decline, the economic picture is never static; unexpected inflation surprises or shifts in the labor market could influence future Fed decisions. Therefore, while the current trajectory suggests a favorable environment for refinancing, remaining vigilant to economic indicators and expert forecasts from institutions like Goldman Sachs is essential for making well-timed decisions that can profoundly impact your financial future.

Conclusion

The question of whether you can you refinance a home equity line of credit is not merely rhetorical; it represents a powerful opportunity for homeowners to optimize their financial position and enhance their wealth management strategy. As Daily98news has explored, refinancing a HELOC can provide substantial benefits,, presents a potentially opportune moment to re-evaluate your existing HELOC terms.

However, such decisions demand a disciplined, data-driven approach, carefully weighing the advantages against the associated costs like closing fees. We encourage Daily98news readers to conduct a thorough analysis of their financial situation, compare offers, and consider their long-term financial objectives. By acting proactively and with an informed perspective, you can confidently navigate the complexities of home equity financing, making choices that contribute to your sustained financial freedom and investment success.

{kind=link}