In the dynamic landscape of personal finance, understanding the levers available to optimize one’s financial position is paramount. For homeowners, a mortgage represents one of the largest financial commitments, and managing it effectively can significantly impact long-term wealth accumulation. Today, let’s join Daily98news to find out exactly how often can you refinance a mortgage, dissecting the underlying financial principles and practical considerations that should guide this crucial decision. This article will provide a comprehensive overview, equipping you with the knowledge to approach mortgage refinancing with strategic foresight and discipline.

Understanding mortgage refinancing

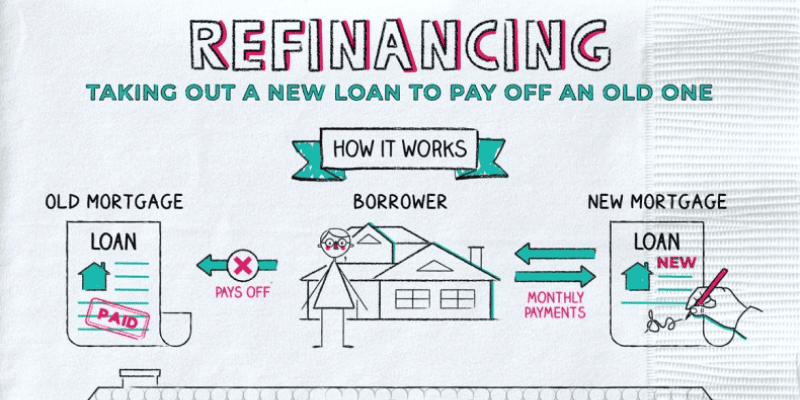

Mortgage refinancing involves replacing an existing mortgage with a new one, typically to secure more favorable terms or to tap into home equity. It is a financial strategy that, when executed judiciously, can lead to substantial savings over the life of the loan or provide much-needed liquidity. While there isn’t a legal limit on how often can you refinance a mortgage, practical financial considerations and market conditions dictate the optimal frequency. A homeowner might consider refinancing for various reasons, including lowering their interest rate, reducing monthly payments, changing the loan term, or consolidating debt. The decision to refinance should always be rooted in a clear financial objective, aligning with one’s broader investment and wealth management strategy.

Key considerations for refinancing frequency

While the concept of refinancing might seem straightforward, the practicalities of how often can you refinance a mortgage involve a blend of financial prudence and market timing. Several factors play a critical role in determining if and when a refinance makes sense, extending beyond merely securing a lower interest rate. A diligent financial analyst would scrutinize these elements to ensure the decision yields tangible, long-term benefits rather than merely incurring additional costs. Understanding these considerations is fundamental to leveraging refinancing as a tool for financial optimization rather than a reactive measure.

The 2% rule and interest rate differentials

A common rule of thumb in the industry suggests that refinancing is generally worthwhile if you can reduce your interest rate by at least 0.75% to 2%. This guideline helps to ensure that the savings generated, if a homeowner has an existing mortgage at 6% and current market rates allow for a refinance at 4.5%, the 1.5% reduction would likely justify the transaction. However, this “rule” is a starting point, not an absolute. A smaller interest rate drop could still be beneficial, especially on a large loan balance or if the homeowner plans to stay in the home for many years, allowing more time for the savings to materialize. The precise breakeven point depends on the specific loan amount, remaining term, and closing costs.

Closing costs and breakeven analysis

Every mortgage refinance comes with a set of closing costs, which typically range from 2% to 5% of the loan principal. These costs can include origination fees, appraisal fees, title insurance, and other administrative charges. To determine if refinancing is financially sound, it is imperative to conduct a breakeven analysis. This involves calculating how long it will take for the monthly savings, if refinancing saves $200 per month and the closing costs are $4,000, the breakeven point is 20 months ($4,000 / $200). If a homeowner plans to sell the property or refinance again before this breakeven point, the refinance might not be a wise financial move, as they would lose money on the transaction.

Loan-to-value (LTV) and equity

Lenders assess risk based on your loan-to-value (LTV) ratio, which is the amount of your mortgage relative to your home’s appraised value. A lower LTV, indicative of substantial home equity, generally makes a borrower more attractive to lenders and can unlock better interest rates and terms. Refinancing frequently without sufficient equity buildup between transactions can be challenging, as lenders often require a minimum LTV, typically 80% or 90%, to avoid requiring private mortgage insurance (PMI). Market fluctuations in home values also play a significant role. A property value increase can improve your LTV, making a refinance more feasible, while a decrease could make it impossible to refinance without bringing cash to the table or accepting less favorable terms.

Credit score and financial health

Your credit score is a critical determinant of the interest rate you qualify for during a refinance. Lenders use credit scores to evaluate your creditworthiness and repayment risk. A higher credit score (typically above 740) signals to lenders that you are a reliable borrower, enabling you to secure the most competitive rates. Fluctuations in your credit score, perhaps due to new debt or late payments, could negatively impact your ability to refinance on favorable terms. Moreover, your overall financial health, including your debt-to-income ratio and employment stability, will be scrutinized. A robust financial profile enhances your chances of a successful and beneficial refinance, underscoring the importance of maintaining strong personal financial discipline.

Strategic reasons to refinance

Beyond merely lowering an interest rate, homeowners consider refinancing for a multitude of strategic financial reasons. Each motivation is rooted in a distinct financial goal, whether it’s enhancing cash flow, accelerating wealth accumulation, or managing existing debt more effectively. Understanding these strategic imperatives helps to frame the decision of how often can you refinance a mortgage within a broader context of personal financial planning.

Lowering your interest rate and monthly payment

This is arguably the most common and compelling reason to refinance. When market interest rates decline significantly since the inception of your original mortgage, securing a new loan at a lower rate can lead to considerable savings over the life of the loan. Even a seemingly small reduction in the interest rate can translate into hundreds or even thousands of dollars in savings annually, freeing up cash flow that can be redirected towards other financial goals, such as investments, retirement savings, or debt reduction. This strategy is particularly effective when coupled with a stable or increasing income, allowing for a strategic adjustment in household budgeting and expenditure.

Changing loan terms

Homeowners might choose to refinance to alter the duration of their mortgage. For instance, moving from a 30-year fixed-rate mortgage to a 15-year fixed-rate mortgage can significantly reduce the total interest paid over the life of the loan and accelerate equity buildup. While this typically results in higher monthly payments, it aligns with a goal of achieving financial freedom sooner. Conversely, extending a loan term, perhaps from a 15-year to a 30-year mortgage, can lower monthly payments, providing crucial financial relief during periods of economic uncertainty or unexpected expenses. This flexibility allows homeowners to adapt their mortgage structure to their evolving financial circumstances and long-term objectives.

Tapping into home equity

A cash-out refinance allows homeowners to borrow against the equity they have accumulated in their home, receiving the difference between the new, larger mortgage and the old one as a lump sum of cash. This capital can be utilized for various purposes, such as funding home renovations, consolidating high-interest debt, investing in other assets, or covering significant life events like education expenses. While this provides access to capital at a potentially lower interest rate than other loan types, it’s essential to use the funds wisely. Using a cash-out refinance for discretionary spending without a clear return on investment can erode home equity and increase overall debt.

Converting an adjustable-rate mortgage (ARM) to a fixed-rate mortgage

Many homeowners initially opt for an adjustable-rate mortgage (ARM) to benefit. Refinancing from an ARM to a fixed-rate mortgage provides stability and predictability, locking in an interest rate for the remainder of the loan term. This strategy offers peace of mind, protecting against potential payment shock from future rate increases and simplifying long-term financial planning. It is a prudent move for those who prioritize payment stability over potential, but uncertain, future rate reductions.

The current market environment and refinancing

The broader macroeconomic environment plays a pivotal role in dictating the feasibility and attractiveness of refinancing. Interest rates, inflation, and the overall housing market are external factors that savvy investors must monitor closely when contemplating how often can you refinance a mortgage. Daily98news emphasizes that a deep understanding of these market forces is crucial for making informed, data-driven decisions that align with your financial goals.

Interest rate trends and projections

Mortgage interest rates are largely influenced by the Federal Reserve’s monetary policy, inflation expectations, and bond market movements. When the Federal Reserve raises or lowers the federal funds rate, it indirectly impacts the cost of borrowing for consumers, including mortgage rates. Historically, periods of economic expansion and low inflation often lead to lower interest rates, making refinancing more appealing. Conversely, inflationary pressures or a tightening monetary policy can drive rates higher, diminishing the immediate benefit of refinancing. Keeping a close watch on economic indicators and central bank announcements is essential for anticipating shifts in the rate environment and timing a refinance effectively.

Impact of inflation on purchasing power

Inflation erodes the purchasing power of money over time, a concept that extends to the value of debt. While rising inflation typically leads to higher interest rates, it can also diminish the real value of fixed-rate mortgage payments. For instance, if you have a fixed-rate mortgage at 4% and inflation is running at 3%, your real interest cost is effectively 1%. However, if you are considering a cash-out refinance, it is crucial to consider that the cash you receive might buy less in an inflationary environment. Investors must weigh the benefits of lower monthly payments against the broader economic landscape and its effects on overall wealth.

Housing market dynamics

The health of the local and national housing market directly impacts home values and, consequently, your loan-to-value ratio. A robust housing market with appreciating property values can improve your equity position, making it easier to qualify for a refinance and potentially securing better terms. Conversely, a declining market can reduce your equity, making a refinance difficult or even impossible without bringing additional funds to the closing table. Monitoring housing market reports, including median home prices, inventory levels, and sales volume, provides valuable context for your refinancing decision. The interplay of supply and demand for housing ultimately influences the financial benefits derived.

Potential downsides and risks of frequent refinancing

While the allure of securing a lower interest rate or better terms is strong, the decision of how often can you refinance a mortgage must also acknowledge the potential pitfalls. Over-reliance on refinancing without a clear strategic purpose can erode financial gains and even put a homeowner in a worse position. A disciplined approach requires a thorough understanding of these risks and how to mitigate them.

Accumulation of closing costs

Each time you refinance, you incur closing costs. While these costs might be rolled into the new loan, effectively avoiding an out-of-pocket expense, they still add to your total debt. Refinancing too frequently means these costs can accumulate over time, potentially negating the savings, if you save $100 a month but incur $5,000 in closing costs every two years, you are essentially losing money in the long run. Prudent financial management dictates that the long-term savings must significantly outweigh the recurring costs to justify the transaction.

Extending the loan term and increasing total interest paid

One common pitfall when refinancing, especially to achieve lower monthly payments, is extending the loan term. For instance, if you’ve paid into a 30-year mortgage for 10 years and then refinance into another 30-year mortgage, you’ve effectively restarted the clock, increasing the total time you’ll be paying off a mortgage to 40 years. This significantly increases the total amount of interest paid over the combined life of the loans, even if the interest rate on the new loan is lower. This strategy should only be employed with a clear understanding of the financial trade-offs and when absolutely necessary for cash flow management.

Negative amortization and payment shock with ARMs

While refinancing from an ARM to a fixed-rate mortgage is often a wise move, repeatedly refinancing between different types of ARMs or not understanding their structure can be risky. Some ARMs include features like negative amortization, where your monthly payments are less than the interest accrued, causing your loan balance to increase over time. Furthermore, an ARM’s interest rate can adjust sharply upwards, leading to significant payment shock if not carefully managed or refinanced into a stable product when rates are favorable. Understanding the intricacies of different loan products is crucial to avoid these financial hazards.

Conclusion

Understanding how often can you refinance a mortgage is less about a hard-and-fast rule and more about a strategic financial assessment. The decision should always be driven by clear financial objectives, a thorough analysis of costs versus benefits, and an awareness of the prevailing market conditions. Daily98news encourages you to approach refinancing with the same discipline and data-driven mindset you apply to your investment portfolio. By carefully weighing the potential savings against the associated costs and risks, homeowners can leverage refinancing as a powerful tool to optimize their financial health, achieve long-term savings, and build sustainable wealth.

{kind=link}