As a homeowner, the equity built in your property is a significant asset, representing a powerful financial tool that can be leveraged for various purposes,. Understanding how to responsibly access this capital is paramount for long-term financial health. The two primary methods for tapping into your home’s equity are a home equity loan vs cash out refinance. Both offer distinct advantages and drawbacks, and choosing the correct path requires a thorough analysis of your financial situation, goals, and the prevailing market conditions. In this article, Daily98news will accompany you to explore these options in depth, providing the clarity needed to make an informed decision for your investment journey.

Understanding Your Home Equity

Home equity is the portion of your home that you truly own. It is calculated as the difference between your home’s current market value and the outstanding balance of your mortgage and any other liens against the property. For example, if your home is valued at $400,000 and you owe $200,000 on your mortgage, you have $200,000 in equity. Building equity typically occurs through consistent mortgage payments, which reduce your principal balance over time, and through appreciation in your home’s market value due to improving real estate conditions or strategic home improvements. This accumulated wealth is not liquid, but it can be converted into cash to meet various financial needs. Lenders generally require you to maintain a certain percentage of equity, often around 20%, to qualify for products that allow you to borrow against your home.

What Is A Home Equity Loan?

A home equity loan, often referred to as a second mortgage, allows you to borrow a lump sum of money against the equity in your home. This loan is separate, meaning you will have two distinct monthly payments: one for your original mortgage and one for the home equity loan. These loans typically come with a fixed interest rate, providing predictable monthly payments over the loan’s term, which can range, one-time financial need.

Advantages of a Home Equity Loan

Home equity loans present several compelling benefits for homeowners. The fixed interest rate is a significant advantage, offering stability and predictability in your monthly payments, which can greatly simplify budgeting over the life of the loan. This contrasts with variable rates that can fluctuate, leading to unpredictable payment adjustments. Additionally, interest rates on home equity loans are generally lower than those on unsecured personal loans or credit cards, as your home serves as collateral, reducing risk for the lender. If the funds are used for home improvements, the interest paid on the loan may also be tax-deductible, offering another potential financial benefit. Furthermore, a home equity loan allows you to retain your existing primary mortgage, which is particularly beneficial if you have a favorable, low interest rate on your original loan that you wish to preserve.

Disadvantages of a Home Equity Loan

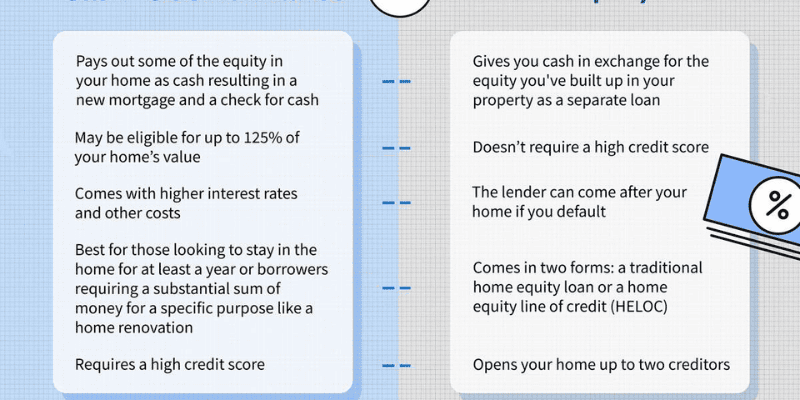

Despite their advantages, home equity loans also carry certain drawbacks. The most significant risk is that your home serves as collateral, meaning that if you default on payments, you could face foreclosure and lose your property. Furthermore, taking on a second mortgage means managing two separate monthly payments, which can complicate your financial planning and increase your overall debt burden. Home equity loans often come with closing costs, similar to a primary mortgage, typically ranging from 2% to 6% of the loan amount, which can add to the upfront expense. While the interest rates are fixed, they tend to be higher than those offered on cash-out refinances because home equity loans are considered a second lien position, making them riskier for lenders in the event of default.

Exploring A Cash-Out Refinance

A cash-out refinance involves replacing your existing mortgage with a new, larger mortgage that includes an additional cash component. This means your original mortgage is paid off, and you secure a single, new loan for a higher amount than your previous balance, with the difference being returned to you in cash at closing. The new loan will come with its own terms, including a new interest rate and repayment schedule, potentially resetting your mortgage clock for another 15 or 30 years. Homeowners often utilize a cash-out refinance when their home’s value has increased significantly or they have accumulated substantial equity, allowing them to access a considerable sum of money for various financial endeavors.

Advantages of a Cash-Out Refinance

Cash-out refinances offer several key advantages. One of the primary benefits is the ability to access a substantial lump sum of cash, often more than what might be available through a home equity loan, by leveraging the accumulated equity in your home. This can be particularly useful for large expenses like extensive home renovations, consolidating high-interest debt, or funding education. Additionally, cash-out refinances typically come with lower interest rates compared to home equity loans because they are a first-lien mortgage, which is less risky for lenders. Consolidating your borrowing into a single mortgage payment can also simplify your finances and potentially lead to a lower overall monthly housing expense if you secure a more favorable interest rate than your original mortgage. Like home equity loans, interest on the refinanced amount used for home improvements can also be tax-deductible.

Disadvantages of a Cash-Out Refinance

While attractive, a cash-out refinance also presents notable drawbacks. The most significant is that it replaces your entire existing mortgage, which could mean losing a favorable, low interest rate you secured years ago if current market rates are higher. As of November 2025, average 30-year fixed refinance rates are around 6.67%. Moreover, taking out a larger loan increases your overall debt burden and extends the repayment term, meaning you could be paying off your mortgage for a longer period and accumulating more interest over the long run. Closing costs for a cash-out refinance are generally higher than for a home equity loan, typically ranging from 2% to 6% of the new, larger loan amount. These costs can significantly reduce the net cash received. The increased loan balance also results in a higher monthly mortgage payment, which could put your home at greater risk of foreclosure if payments become unmanageable. Furthermore, cash-out refinance rates are generally higher than rates for a standard rate-and-term refinance due to the increased risk associated with a higher loan-to-value (LTV) ratio. Lenders often require you to maintain at least 20% equity after the refinance, capping the amount you can borrow.

Key Differences: Home Equity Loan Vs Cash-Out Refinance

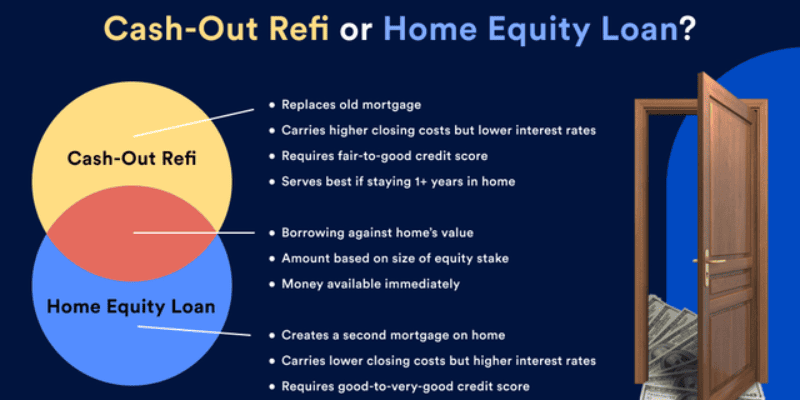

The fundamental distinction between a home equity loan vs cash out refinance lies in their structure and impact on your existing mortgage. A home equity loan functions as a second mortgage, leaving your original mortgage intact with its current terms and interest rate. This means you manage two separate loan payments each month. In contrast, a cash-out refinance replaces your entire existing mortgage with a new, larger one that encompasses both your old balance and the new cash amount, resulting in a single new mortgage payment.

Interest rates also differ significantly. Home equity loans typically feature fixed interest rates, providing payment stability, but these rates are often higher than those on a cash-out refinance due to their subordinate lien position. Cash-out refinances, being a first-lien mortgage, generally offer more competitive, lower interest rates, although these rates will apply to the entire new, larger loan amount. Closing costs for home equity loans are generally lower than for cash-out refinances. The decision largely depends on whether you wish to preserve your existing mortgage’s interest rate and terms, or if you prefer consolidating your debt into a single, potentially lower-rate, but larger, new mortgage.

Choosing The Right Option For Your Financial Goals

Deciding between a home equity loan vs cash out refinance hinges on your specific financial objectives and current market conditions. If you have an excellent interest rate on your current mortgage that you want to preserve, a home equity loan is often the more suitable choice. This allows you to tap into your equity without disturbing your favorable first mortgage terms. It is also ideal if you need a specific, one-time lump sum for a project like a home renovation, offering predictable fixed payments. The lower closing costs associated with home equity loans can also make them more appealing for smaller borrowing needs.

Conversely, a cash-out refinance may be more advantageous if current interest rates are significantly lower than your existing mortgage rate, offering an opportunity to reduce your overall borrowing costs while simultaneously accessing cash. This option is also beneficial if you aim to consolidate multiple high-interest debts, streamlining your finances into a single, potentially lower-rate mortgage payment. However, careful consideration of the increased loan balance and reset loan term is crucial. Ultimately, align your choice with whether you prioritize preserving your current mortgage or optimizing your overall mortgage rate and payment structure for a larger sum of cash.

Risks And Considerations For Both Options

Regardless of whether you choose a home equity loan vs cash out refinance, both options carry inherent risks that demand careful consideration. The most significant risk for both is that your home serves as collateral. Failure to make timely payments on either a home equity loan or a cash-out refinance can lead to foreclosure, potentially resulting in the loss of your home. This fundamental risk underscores the importance of a robust financial plan and a clear understanding of your repayment capacity before committing to either option.

Another crucial factor is the impact on your debt-to-income (DTI) ratio. Taking on additional debt through either method will increase your DTI, which lenders use to assess your ability to manage monthly payments. A higher DTI could affect your ability to secure other forms of credit in the future. Closing costs are also a reality for both, though they tend to be higher for a cash-out refinance. These upfront expenses can reduce the net amount of cash you receive, so it is vital to factor them into your calculations. Furthermore, market interest rate fluctuations can influence the attractiveness of either option. While home equity loans offer fixed rates, cash-out refinances are subject to prevailing mortgage rates, which have seen considerable movement in recent years. For example, 30-year fixed mortgage rates, which dipped below 3% in 2020-2021, surged in 2022 to over 7% before settling around 6.35% in November 2025. Always assess your personal financial stability and the broader economic climate before making a decision that ties into your most significant asset.

Final Thoughts

The decision between a home equity loan vs cash out refinance is a complex one, deeply intertwined with your individual financial landscape and long-term aspirations. As we at Daily98news have explored, each option provides a distinct pathway to unlock the value embedded in your home, but each also comes with its unique set of benefits and considerable risks. A home equity loan preserves your existing first mortgage and offers predictable, fixed payments on a separate loan, ideal for specific, one-time funding needs. A cash-out refinance, on the other hand, replaces your entire mortgage, potentially allowing for lower interest rates on a larger sum and simplified payments, though at the cost of resetting your loan term and incurring higher closing costs. Responsible financial stewardship demands that you meticulously evaluate your current mortgage rate, your borrowing needs, your comfort with managing multiple payments versus a single larger one, and your tolerance for risk. By understanding these nuances, you can confidently make a data-driven decision that aligns with your financial goals, ensuring that leveraging your home’s equity serves as a strategic move towards wealth accumulation and financial freedom, rather than a source of unforeseen burden.

{kind=link}